PrOrumah Policy Document

- OUR AGREEMENT

- WHAT MAKES UP THIS POLICY

- YOUR DUTY TO INFORM US

- INSURING CLAUSE (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

- APPLICABLE WARRANTIES (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

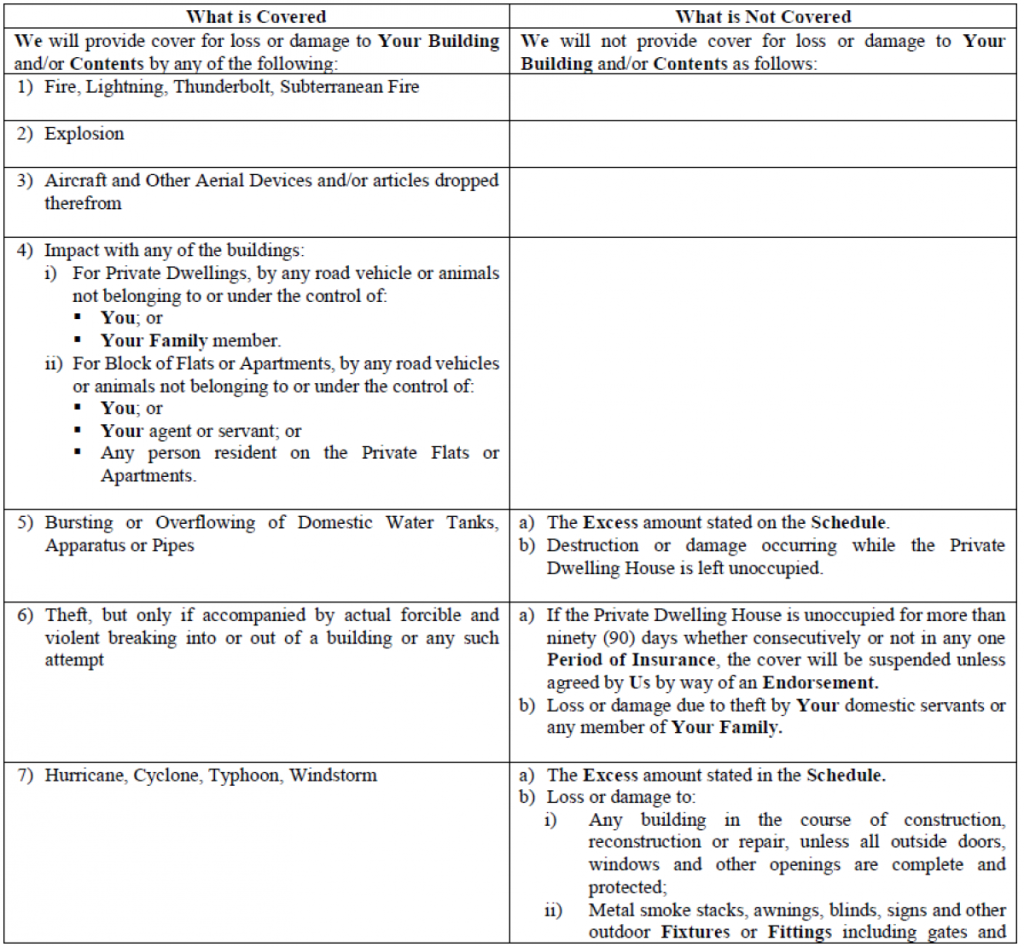

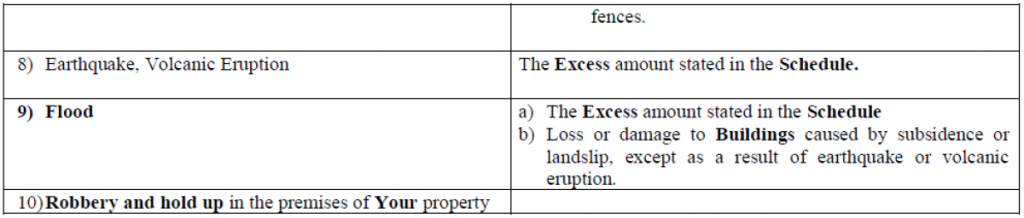

- INSURED EVENTS (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

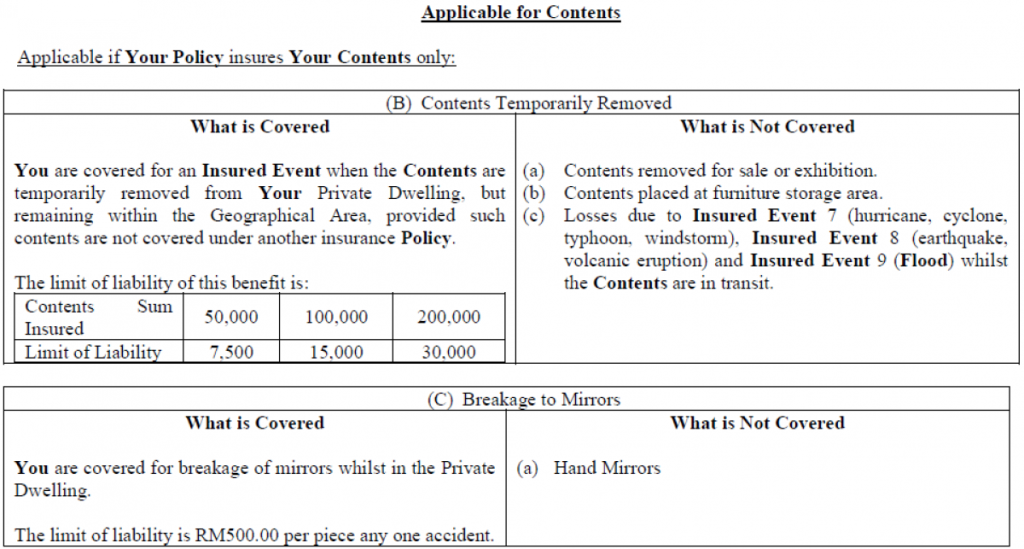

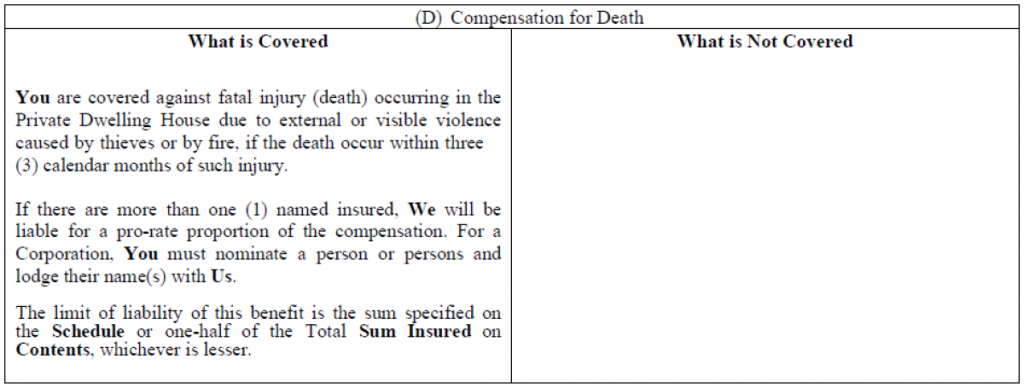

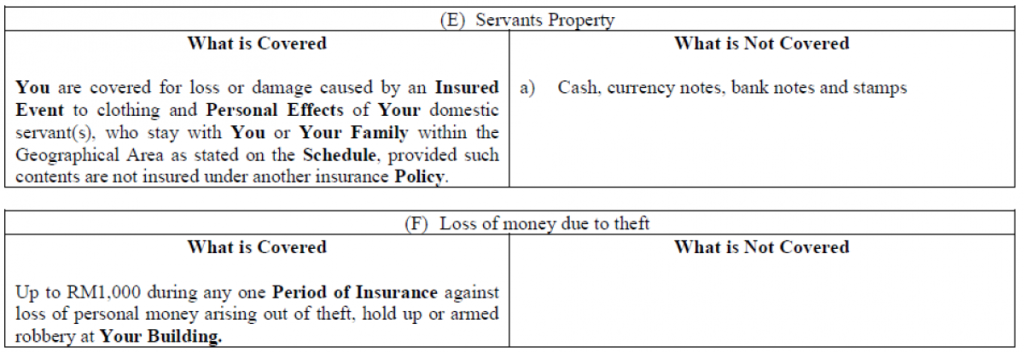

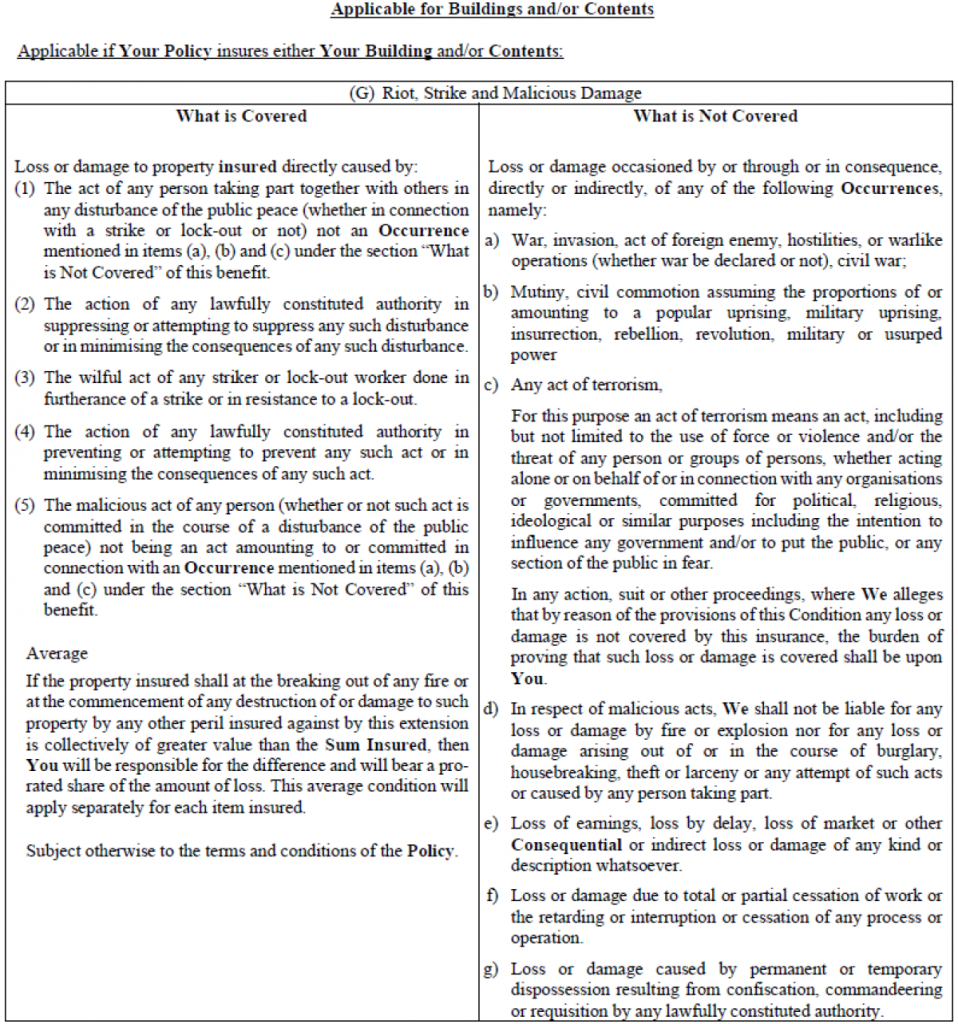

- ADDITIONAL BENEFITS

- GENERAL EXCEPTIONS (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

- HOW WE WILL SETTLE YOUR CLAIM (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

- HOW TO MAKE A CLAIM (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

- YOUR RESPONSIBLITY (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

- HOW YOUR POLICY MAY BE CANCELLED (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

- GLOSSARY

- OPTIONAL BENEFITS

OUR AGREEMENT

WHAT MAKES UP THIS POLICY

YOUR DUTY TO INFORM US

INSURING CLAUSE (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

We will insure the Buildings and/or Contents as shown on Your Schedule during the Period of Insurance.

This cover will be given on the basis that You agree to pay Us the Premium for the cover.

In respect of Insured Events occurring during the Period of Insurance and subject to the limitations, exceptions and conditions contained or endorsed in the Policy, We will, by payment or by reinstatement or repair, indemnify You against loss or damage to the property insured as mentioned in the Schedule.

This Policy insures You up to the amount of the Sum Insured as stated in the Schedule for loss or damage to Your Buildings and/or Your Contents caused by an Insured Event.

Your Schedule will show if You have insured Your Building, Your Contents or both.

Your Building

“Buildings” means buildings of a Private Dwelling House at the Premises and includes:

- all domestic offices, stables;

- garages and outbuildings on the same Premises used solely in connection to it and on the same Premises;

- Fixtures and Fittings;

- walls, gates and fences around the Premises.

Private Dwelling House shall also refer to buildings of Flats and Apartments.

When Blocks of Flats or Apartments are insured, Private Dwelling House will refer to the Private Flats or Apartments.

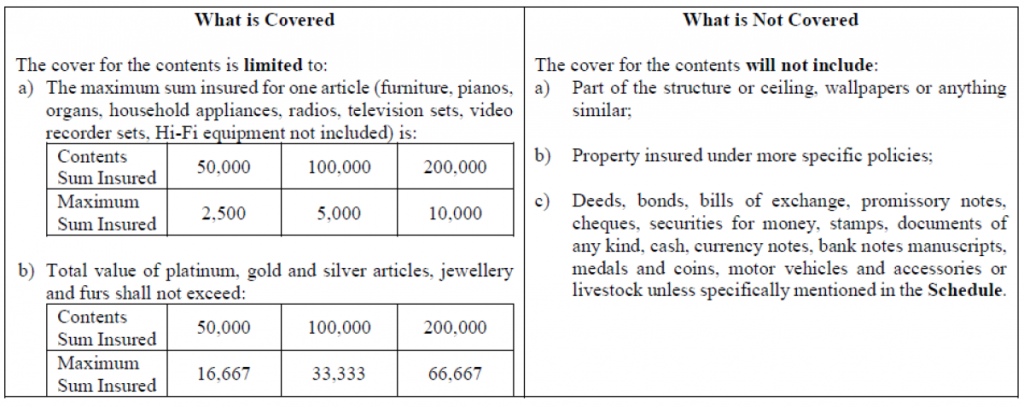

Your Contents

“Contents” means Household goods and Personal Effects of every description, belonging to You or any member of Your Family normally residing with You contained in the Private Dwelling House, Flat or Apartment and all domestic offices, stables, garages and out-buildings, used solely in connection to it, on the same Premises specified on the Schedule.

APPLICABLE WARRANTIES (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

INSURED EVENTS (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

ADDITIONAL BENEFITS

This refers to additional benefits provided to You without any additional Premium, but which are subject to the terms and conditions of the Policy.

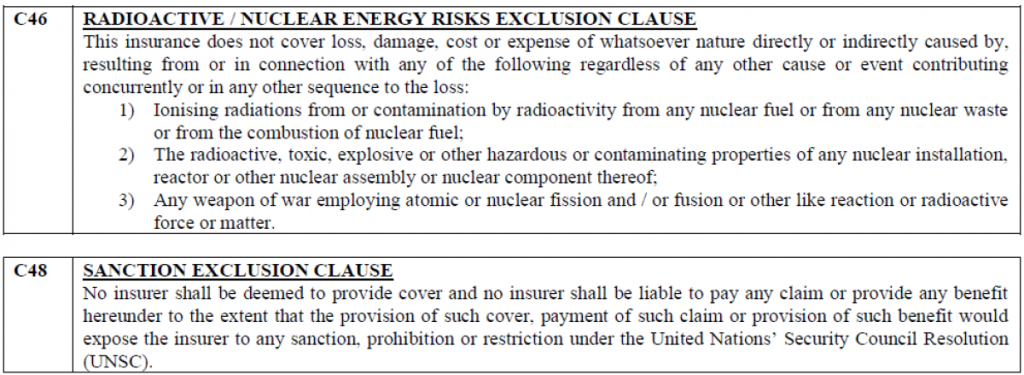

GENERAL EXCEPTIONS (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

HOW WE WILL SETTLE YOUR CLAIM (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

HOW TO MAKE A CLAIM (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

YOUR RESPONSIBLITY (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

HOW YOUR POLICY MAY BE CANCELLED (APPLICABLE FOR BUILDINGS AND/OR CONTENTS)

GLOSSARY

Some words and expressions in this Policy have a specific meaning which is given below. Each word is printed in bold where it appears.

“Consequential loss” means financial loss.

“Consumer Insurance Contracts” means insurance wholly for purposes unrelated to the Insured’s trade, business or profession.

“Depreciation” means the reduction in the value of the item or property due to Wear and Tear.

“Endorsement” means a written alteration to the terms, conditions and limitations of this Policy which is shown on the Schedule.

“Erosion” means being worn or washed away by water or wind.

“Excess” means the amount You must pay towards a claim before We pay. The amount will be stated on the Schedule or in any selected Optional Benefits.

“Flood” means the overflowing or deviation from their normal channels of either natural or artificial water courses, bursting or overflowing of public water mains and any other flow or accumulation of water originating from outside the building.

“Family” and “Household” means any person(s) who normally reside with You.

“Fixtures” and “Fittings” means items that are permanently attached to Your Building.

“Indemnity” means putting You back to Your same financial position immediately before the loss.

“Insured Event” means one of the perils listed under this Policy.

“Non-Consumer Insurance Contracts” means insurance for purposes related to the Insured’s trade, business or profession.

“Occurrence” means the exact period when the incident took place.

“Open” means anywhere at the Premises not fully enclosed by walls and a roof and which is not able to be Secured, also any outbuildings on the Premises if such Buildings are not able to be Secured.

“Period of Insurance” means the period for which You are insured. It commences at the time We agree to give You insurance and finishes at midnight on the day of expiry. The expiry date is shown on the Schedule.

“Personal Effects” means personal items regularly worn or carried on the person for his/her personal use, for example clothing, watch, wallet.

“Plate Glass” means glass fitted to the structure of the building.

“Policy” means Your insurance contract which consists of this policy wording and Schedule.

“Premium” means any amount We require You to pay under the Policy and includes Government charges.

“Premises” means the land at the address shown on the Schedule on which the building is built, including the yard or garden used only for domestic purposes.

“Robbery and hold up” means that the items insured are either taken away or surrended; in both instances due to force, menaces or threat of physical violence made against You, or persons living with You in a common household, or other persons authorized to be on Your premises.

"Schedule” means the Policy Schedule where both the insured items and sum insured are specified.

“Secured” means locked so as to prevent entry other than by using force.

“Sum insured” means the amount You have insured on either Your Building, Your contents (including specified Contents) as shown on the Schedule. This shall include the Additional Benefits and any of the Optional Benefits selected by You.

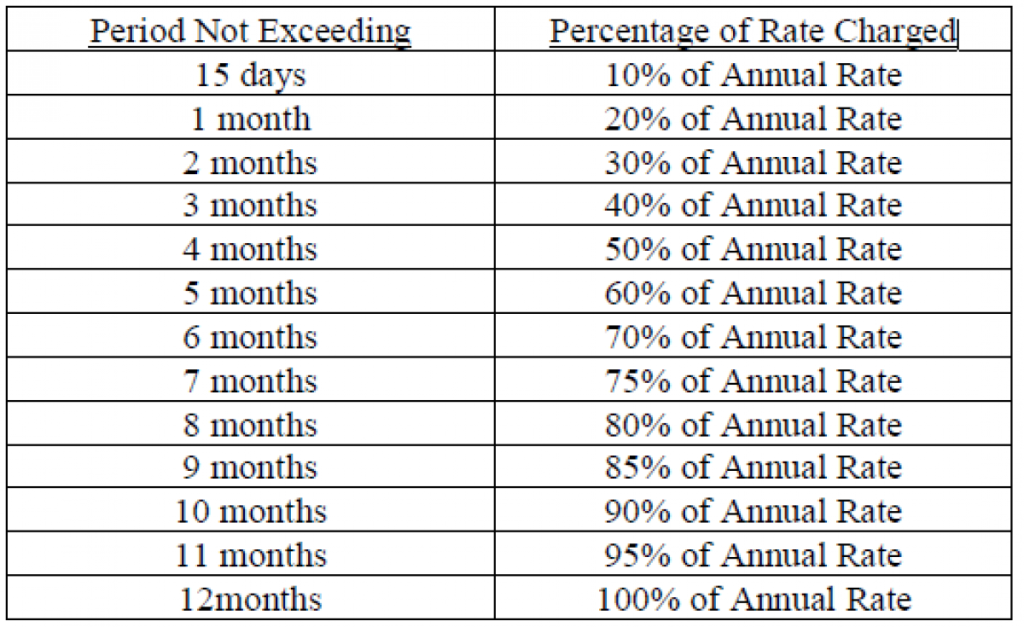

“Customary short-period rates” means the following:

“Warranties” means either restriction or obligation that the Policy imposes on You. A breach of a warranty will entitle Us to reject the claim for loss or damage or liability.

“Wear and tear” means damage or a reduction in value through age, ordinary use or lack of maintenance.

“We, Our and Us” means the insurance company.

“You and Your” means the person(s) named on the Schedule as the insured.

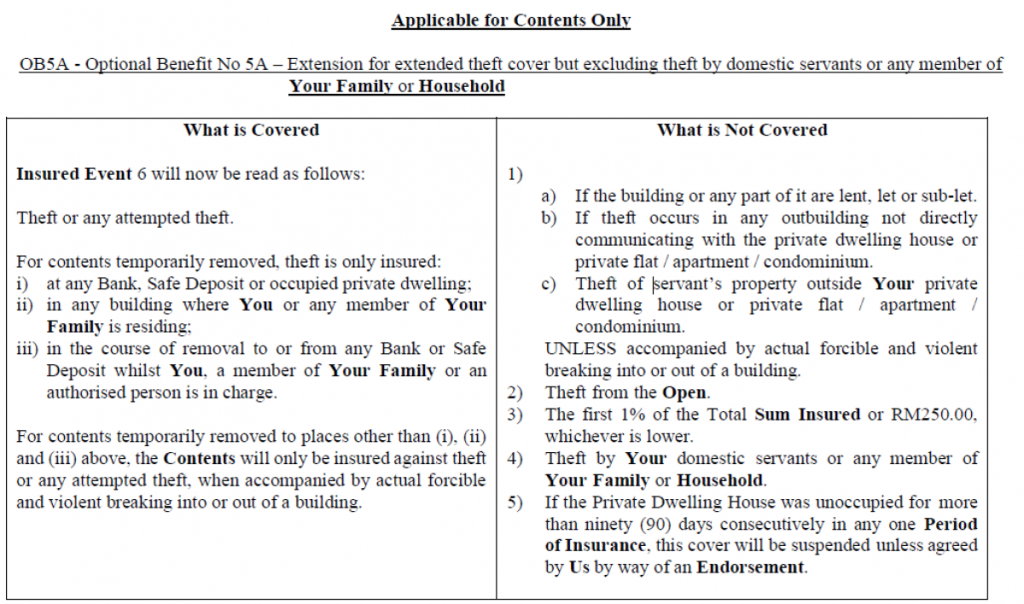

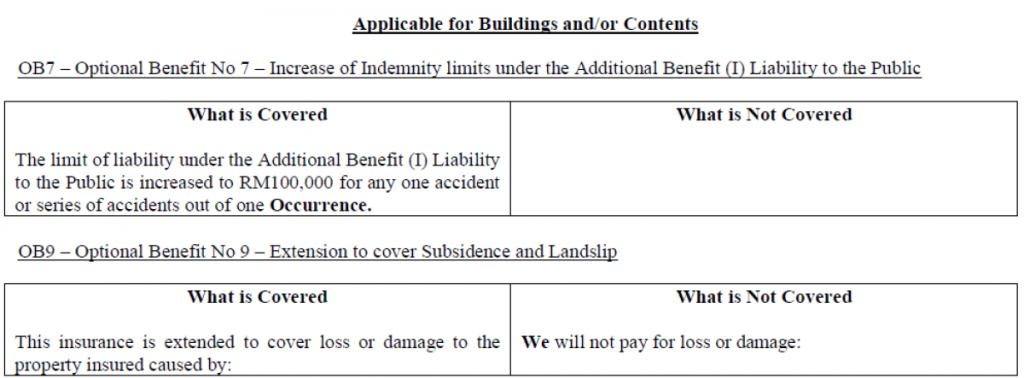

OPTIONAL BENEFITS

For an additional Premium, Your Policy may be extended to cover the following benefits to the insured Buildings and/or Contents. These optional benefits will be stated on the Schedule if You choose to take these up.

NOTICE

For all intents and purposes where there is a conflict or ambiguity as to the meaning in the Bahasa Malaysia provisions of any part of the Contract, it is hereby agreed that the English version of the Contract shall prevail.